The Reality of Life After Selling Your Financial Advisory Firm

Selling your financial advisory firm is only part of the transition. While advisors often spend years preparing for valuation, due diligence, and...

11 min read

Financing an advisory firm acquisition involves much more than securing the capital to complete the purchase. The most successful transactions use a financing structure that balances cash flow, aligns the interests of the buyer and seller, and supports a smooth transition after closing. Whether the deal includes SBA lending, seller financing, earnouts, or private capital, the right approach can improve deal certainty and position the combined firm for long-term success.

As competition for advisory firms continues to increase, acquisition financing has become a key differentiator for buyers. ECHELON Partners reported that wealth management M&A deal volume reached a record 466 transactions in 2025, up 27% year over year, with activity supported in part by a lower and more stable cost of capital. Buyers now need more than access to funding. They need financing strategies that preserve cash flow, strengthen negotiations, and support sustainable growth after closing.

Whether you're acquiring another advisory practice or preparing your own business for sale, understanding how advisory firm acquisitions are financed helps both buyers and sellers negotiate more effectively, reduce transaction risk, and structure deals that protect long-term business value.

A successful advisory firm acquisition depends on more than agreeing to the right purchase price. The financing structure behind the transaction influences whether the buyer can sustain future growth, whether the seller receives reliable payment, and whether the combined firm can transition successfully after closing. When financing is poorly structured, even an attractive deal can create unnecessary financial strain, prolonged negotiations, or integration challenges.

The strongest transactions align financing with the broader objectives of both parties. Rather than relying on a single funding source, buyers often combine financing options to preserve cash flow, manage risk, and create a deal structure that supports long-term business performance. For sellers, evaluating how a buyer plans to finance the acquisition provides valuable insight into the likelihood of a successful closing and post-sale continuity.

Financing decisions shape far more than how an acquisition is paid for. They affect liquidity, debt obligations, transition planning, and the buyer's ability to continue investing in the business after closing. Sellers, meanwhile, must balance achieving an attractive purchase price with confidence that the buyer has the financial capacity to fulfill the terms of the purchase agreement.

No single financing structure works for every acquisition. The right approach depends on the advisory firm's valuation, financial performance, growth potential, and the goals of both the buyer and the seller. Successful acquirers view financing as a strategic component of the transaction rather than simply a way to fund the purchase.

Read More: Understanding Valuation Multiples for a Financial Advisor Practice

Although buyers and sellers share the objective of completing a successful transaction, they often evaluate financing from different perspectives. Buyers typically focus on affordability, cash flow, and financial flexibility after closing. Sellers are more concerned with payment certainty, transaction risk, and confidence that the acquiring firm has the financial strength to support clients, employees, and future growth.

Recognizing these priorities early creates stronger negotiations and better transaction outcomes. Financing terms influence everything from seller financing and earnouts to transition timelines and the overall deal structure. When both parties understand how financing affects the broader acquisition strategy, they are better positioned to negotiate an agreement that supports long-term value for everyone involved.

Advisors evaluating acquisition opportunities can work with Advisor Legacy's Deal Support services, which help buyers and sellers evaluate transaction structures, navigate due diligence, and develop financing strategies aligned with their long-term objectives.

Read Next: Financial Buyer vs Strategic Buyer: How the Right Choice Impacts Your Exit

There is no single financing strategy for every advisory firm merger or acquisition. The strongest transactions are structured around the firm's valuation, assets under management (AUM), cash flow, growth potential, and the long-term objectives of both the buyer and the seller. Whether the goal is acquiring another practice or expanding an established financial advisory business, financing should support not only the purchase itself but also the firm's ability to grow after closing.

Rather than relying on a single funding source, many successful acquisitions combine multiple financing options to reduce risk, preserve liquidity, and create a deal structure that supports long-term business performance. Understanding when each financing strategy works best helps buyers negotiate with greater confidence while assuring sellers that the transaction is built for long-term success.

SBA loans remain one of the most common financing options for qualifying advisory firm acquisitions, particularly for first-time buyers and smaller transactions. Because these loans are partially guaranteed by the U.S. Small Business Administration, lenders may offer longer repayment terms and lower down payment requirements than conventional financing, making ownership more accessible for qualified buyers.

SBA financing can significantly reduce the amount of capital required at closing, but it also involves a detailed diligence process. Buyers should expect lenders to review financial statements, cash flow, AUM, and the overall viability of the advisory practice before approving financing. Buyers with an established relationship with a bank may also benefit from a more efficient lending process, although underwriting requirements remain rigorous.

Seller financing continues to play a central role in advisory firm mergers and acquisitions because it creates flexibility for both parties. Instead of receiving the entire purchase price at closing, the seller finances a portion of the acquisition and receives repayment over an agreed period.

For buyers, seller financing reduces upfront capital requirements while preserving liquidity during the transition. For sellers, it demonstrates confidence in the future performance of the advisory practice and can help bridge valuation gaps during negotiations. Well-structured agreements clearly define repayment schedules, interest rates, default provisions, and other purchase agreement terms, creating greater certainty throughout the transaction.

Read More: How to Structure Seller-Financed Notes: A Step-by-Step Guide for Business Sellers

Earnouts are commonly used when buyers and sellers have different expectations about future growth or valuation. Rather than paying the full purchase price at closing, part of the consideration is tied to measurable business performance after the acquisition.

This approach can be particularly effective when client retention, recurring revenue, or other growth objectives represent a meaningful portion of the firm's projected value. However, successful earnouts depend on clearly defined performance metrics, reporting expectations, and timelines. Establishing these terms before closing reduces the likelihood of disputes and helps both parties negotiate from a shared understanding of success.

Read More: Using Valuation to Negotiate Earnout Terms in Advisory M&A Deals

Experienced buyers with strong financial profiles may choose conventional bank financing instead of SBA lending. Commercial banks often provide greater flexibility for larger acquisitions, particularly when borrowers have established banking relationships, strong liquidity, and a proven history of operating successful financial advisor practices.

Unlike SBA financing, conventional lending typically depends more heavily on the buyer's financial strength, collateral, and borrowing history. Buyers should evaluate lending terms carefully to ensure repayment obligations remain manageable while continuing to invest in client service, technology, and future growth. Lenders also assess revenue or EBITDA to determine how much debt the business can reasonably support after closing.

As M&A activity across the wealth management industry continues to grow, larger acquisition deals increasingly involve private capital alongside traditional financing. Strategic buyers, existing ownership groups, family offices, private investors, and private equity-backed firms may all participate depending on the size and complexity of the transaction.

These financing structures can provide greater flexibility while creating operational synergy between organizations, but they also introduce additional stakeholders whose investment objectives should align before closing. Clearly defining governance, decision-making authority, and long-term growth expectations helps create a stronger foundation for a successful integration.

Successful advisory firm mergers and acquisitions rarely depend on a single financing source. The strongest M&A transactions combine multiple financing options to preserve cash flow, support client retention, and create a smooth transition for both the buyer and the seller. Financing should always be viewed as part of the overall M&A strategy rather than simply a way to fund the purchase. Buyers who evaluate financing early in the acquisition process are better positioned to negotiate effectively, reduce transaction risk, and complete acquisitions that support long-term business growth.

Read Next: Funding A Financial Advisor Practice Acquisition

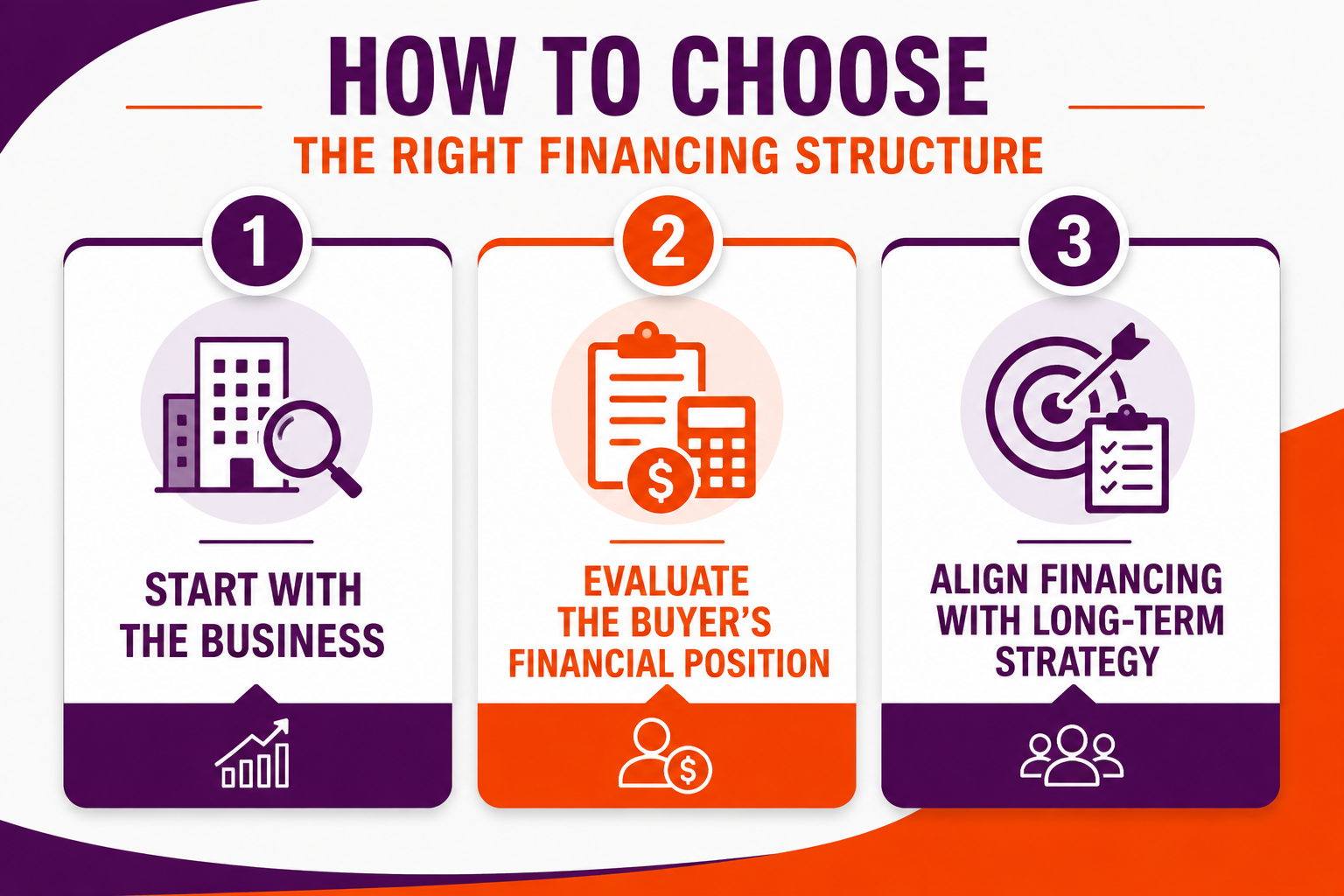

Choosing the right financing structure is about more than finding the lowest interest rate or the largest loan. Every advisory firm acquisition has unique financial characteristics, transaction goals, and risk considerations that influence how the deal should be structured. The strongest financing strategies support not only a successful closing but also the buyer's ability to grow the business and the seller's confidence that the transaction will perform as expected after closing.

Rather than asking which financing option is "best," experienced buyers evaluate which structure creates the strongest long-term outcome for everyone involved. Likewise, sellers should assess financing proposals based not only on purchase price but also on the buyer's financial capacity, transition plan, and ability to sustain the advisory practice after the acquisition.

Every financing decision begins with understanding the business being acquired. Lenders, investors, and buyers evaluate recurring revenue, assets under management (AUM), cash flow, profitability, and overall financial performance to determine how much debt the business can reasonably support.

Financial metrics alone, however, rarely tell the whole story. Client retention, the firm's service model, operational maturity, and future growth opportunities all influence financing decisions because they affect the long-term stability of the business. Advisory firms with predictable recurring revenue and diversified client relationships are often better positioned to secure favorable financing terms.

Read More: Why the Quality of Recurring Revenue Matters in Advisory Firm Acquisitions

The financing structure should fit the buyer just as well as it fits the business. Lenders assess liquidity, borrowing capacity, management experience, and existing debt obligations to determine whether the buyer can successfully complete and operate the acquisition.

Buyers with strong financial statements and established banking relationships may qualify for more flexible lending options, while newer buyers often benefit from combining SBA financing, seller financing, or other funding sources. Understanding these limitations before negotiations begin allows buyers to structure more realistic offers and avoid unnecessary delays during due diligence.

Read More: How To Build A Lender-Ready Valuation Report For Your Advisory Practice

The best financing structures support the long-term objectives of both parties rather than simply funding the purchase. Buyers may prioritize preserving working capital for future acquisitions, technology investments, or talent retention, while sellers often focus on payment certainty, transition stability, and protecting client relationships throughout the ownership change.

Financing should also complement the broader deal structure. Transition timelines, earnouts, seller financing arrangements, and post-sale involvement all influence how the transaction is ultimately structured. When financing aligns with these broader objectives, negotiations become more productive, and the transition is more likely to succeed.

There is no universal financing structure for advisory firm acquisitions. The strongest transactions balance the financial realities of the business with the objectives of both the buyer and the seller. Evaluating these factors early helps reduce financing risk, improve due diligence, and create a smoother path from negotiations to closing.

Financing an advisory firm acquisition is about more than securing the capital to close the transaction. The strongest buyers treat financing as part of their overall M&A strategy, aligning funding decisions with valuation, due diligence, integration planning, and long-term business goals. A well-prepared financing strategy reduces uncertainty during negotiations while positioning both the buyer and seller for a smoother transition after closing.

Rather than viewing financing as the final step before signing a purchase agreement, successful acquirers begin planning early, evaluate multiple financing scenarios, and seek experienced guidance throughout the transaction.

The most successful acquisitions begin long before a letter of intent is signed. Buyers who understand their borrowing capacity, available financing options, and lender expectations are better equipped to negotiate realistic purchase terms and move through due diligence efficiently.

Early planning also benefits sellers by providing greater confidence that financing will not delay or derail the transaction. Identifying potential financing challenges upfront creates a more predictable acquisition process for everyone involved.

Financing should never be considered in isolation. Purchase price, valuation, seller financing, earnouts, transition timelines, and post-sale responsibilities all influence one another. Evaluating these components together helps buyers preserve cash flow while giving sellers greater confidence that the agreed-upon terms can be fulfilled.

The most effective acquisition structures balance affordability with long-term business performance. Rather than maximizing one element of the transaction, successful buyers focus on creating a financing strategy that supports sustainable growth, client continuity, and operational stability after closing.

Financing is only one part of a successful advisory firm acquisition. Buyers and sellers must also evaluate valuation, conduct financial and operational due diligence, negotiate purchase agreements, and develop transition plans that protect client relationships and business continuity.

Experienced transaction advisors help coordinate these moving pieces while ensuring financing decisions align with the broader acquisition strategy. Their guidance can help identify financing alternatives, reduce transaction risk, and create a stronger foundation for long-term success.

Advisors preparing for an acquisition can work with Advisor Legacy's Deal Support and Lending Support services to evaluate financing structures, prepare for due diligence, and navigate complex advisory firm transactions with greater confidence.

Read Next: How to Prepare Your Advisory Firm for Buyer Due Diligence

Financing is much more than a way to fund an advisory firm acquisition. It is one of the key decisions that shapes how the transaction is negotiated, how smoothly ownership transitions, and how successfully the business performs after closing. The right financing structure balances the buyer's growth objectives with the seller's expectations while creating a foundation for long-term stability, client continuity, and enterprise value.

Whether the transaction relies on SBA lending, seller financing, earnouts, conventional bank financing, or a combination of financing strategies, success ultimately comes from aligning the financing structure with the firm's valuation, cash flow, and long-term business goals. Buyers and sellers who begin these conversations early are better positioned to negotiate with confidence, reduce transaction risk, and complete acquisitions that benefit both parties.

Key Takeaways

Financing structure should support the long-term success of the business, not just the closing of the transaction.

Most advisory firm acquisitions combine multiple financing options to balance flexibility, cash flow, and risk.

Buyers should evaluate financing alongside valuation, due diligence, and integration planning rather than as a separate decision.

Sellers should assess a buyer's financing strategy as carefully as the purchase price.

Early planning creates stronger negotiations, smoother transitions, and greater confidence for everyone involved.

Whether you're acquiring another advisory practice or preparing your own firm for sale, financing should be treated as a strategic part of your overall transaction plan. A thoughtful financing approach helps protect business value, supports smoother negotiations, and creates a stronger foundation for long-term success after closing.

Advisors who need guidance evaluating financing structures, preparing for due diligence, or navigating complex transactions can work with Advisor Legacy's Deal Support, Business Valuation, and Lending Support services, which provide strategic support throughout the acquisition process.

Ready to finance your next acquisition with confidence? Schedule a transaction strategy discussion with Advisor Legacy to evaluate your financing options, strengthen your deal structure, and prepare for a successful transition.

Most advisory firm acquisitions use a combination of financing options rather than a single funding source. Common acquisition financing methods include SBA loans, conventional bank financing, seller financing, earnouts, and private capital. The right structure depends on the advisory practice's valuation, cash flow, AUM, and the financial goals of both the buyer and the seller.

Valuation plays a central role in determining how an acquisition is financed. Lenders and investors evaluate financials, recurring revenue, cash flow, EBITDA, and assets under management (AUM) when assessing lending capacity. Using an appropriate valuation method also helps buyers and sellers negotiate financing terms that reflect the firm's long-term value.

Yes. Seller financing is one of the most common financing strategies used in advisory firm mergers and acquisitions. It can reduce the buyer's upfront capital requirements while giving the seller confidence in the future performance of the business. A well-drafted purchase agreement should clearly define repayment terms, interest rates, and any performance-based provisions.

Before choosing a financing structure, buyers should evaluate their liquidity, borrowing capacity, long-term cash flow, and expected return on investment. They should also consider how the financing strategy supports due diligence, the transition timeline, client retention, and the overall M&A process to improve the likelihood of a smooth transition after closing.

Yes. Private equity firms and other investment partners may participate in larger or more complex acquisitions, particularly when buyers are pursuing significant growth opportunities. While private equity can provide additional capital and financial flexibility, buyers should ensure that all stakeholders share similar long-term objectives for governance, growth, and the future direction of the advisory practice.

Selling your financial advisory firm is only part of the transition. While advisors often spend years preparing for valuation, due diligence, and...

Many financial advisors view internal succession as the ideal way to transition their business. It preserves client relationships, protects the...

Financing an advisory firm acquisition involves much more than securing the capital to complete the purchase. The most successful transactions use a...